Digital Currency Electronic Payment, A Brief Interpretation Helping Freshman Grasp the Central Bank’s Digital Currency DCEP

On the afternoon of May 11, 2020, invited by Shenzhen Information Service Blockchain Association and Milin Finance, Xu Chaoyi, founder of Hashi Technology, attended the current Shenzhen Blockchain Week online, telling about “ DCEP and the new era of industrial blockchain. “

The following is the full text of sharing:

Thank you for your invitation. I am Xu Chaoyi from BKFUND and Hashi Technology-Hashgard Blockchain. I am very happy to participate in the first theme forum of Shenzhen Blockchain Week online today. The theme I share with you today is “DCEP and The New Era of Industrial Blockchain.”

We know that on the evening of April 14th last month, a very important thing happened in the circle. Several screenshots of the Agricultural Bank’s DCEP wallet appeared on the Internet. At first, many people thought it was a forgery. On the other hand, a few days ago, people from the central bank came out to confirm the news, saying that the digital currency DCEP has been tested in Suzhou, Xiong’an, Chengdu, and Shenzhen.

In other words, it has been 6 years since the central bank started to study digital currency in 2014, and finally our people have the opportunity to explore the true face of DCEP.

It is quite a complicated topic to fully explain clearly about DCEP, which involves monetary policy, economics, finance, payment, RMB internationalization, cross-border trade, blockchain technology, etc., which may need to be spent a few days and nights, but because most of them do not have much direct relationship with our ordinary people, today on this occasion, we will use payment as the main clue to discuss three issues:

The first question, what exactly is DCEP; the second question, what exactly has DCEP changed; the third question, what opportunities does DCEP mean for our blockchain practitioners?

01 What exactly is DCEP?

Let’s compare DCEP with the commonly used bank accounts, WeChat, and Alipay. If you have 319 yuan, you only record a 319 yuan number in your bank account, WeChat, and Alipay. However, this is not the case for DCEP. If you have a DCEP of 319 yuan, you actually have 3 DCEP of 100 yuan, 1 DCEP of 10 yuan, and 9 DCEP of1 yuan in your DCEP account. Everyone will wonder, is DCEP the same thing as using paper money and banknotes? That ’s right, this is the essential difference between DCEP and WeChat, Alipay, and bank accounts. DCEP is not an electronic currency, but a real electronic RMB. It is the replacement of M0, what is M0, M0 is the cash and banknotes in circulation.

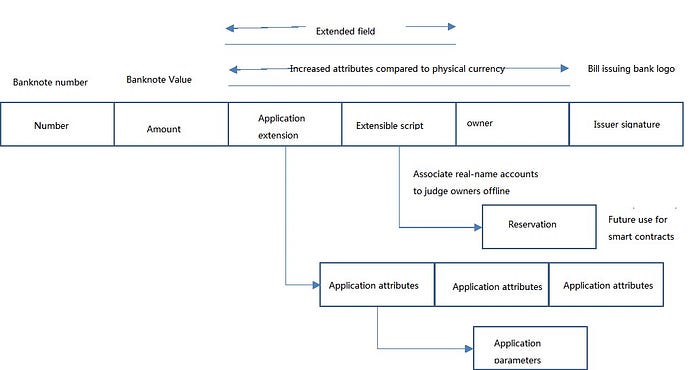

If we decrypt the DCEP string, we can further see its data structure, which consists of a number of different fields, where the number, amount, and issuer signature are similar to our banknote number, face value, and bank issuer in the banknote .

At present, we can understand the bank as a central bank, but in the future there may be more than one bank with the right to issue banknotes.

In addition, some additional fields have been added. The owner field, which identifies the current holder of DCEP, can be anonymous, but it will correspond to the real user in the central bank ’s back-end system, and can determine whether the owner of the currency have the right to make transfers in the dual offline state?

The extensible script is reserved for subsequent use in smart contracts. The extended attributes of the application include currency management attributes, currency security attributes, currency application attributes, registration status attributes, etc. Different attribute values are set by different management agencies. In order to manage the authenticity, uniqueness, circulation status, security status and other functions of the currency, only users who have the right to view the corresponding fields can decrypt it. Unauthorized users can only see the encrypted characters without seeing the original attribute values .

With the field of application extended attributes, the central bank will be able to issue DCEP more flexibly in the future. For example, it is required that the money issued to commercial banks must flow into the manufacturing industry. It can be used to buy machinery and equipment, purchase raw materials, pay workers’ wages, etc. From this point of view, DCEP is not only the electronic RMB, but also a “super currency” and “smart currency” that can be traced, anti-counterfeiting, directional circulation, and can load smart contracts. Its birth will bring revolutionary changes to all aspects of our country.

02 What exactly has DCEP changed?

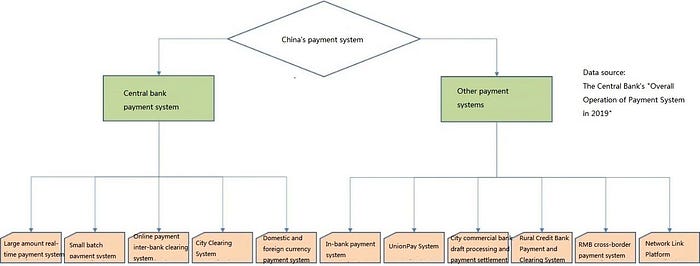

As mentioned earlier, today ’s sharing, we will focus on the main clue of payment. We believe that the most significant change brought about by DCEP is the change in China ’s payment field and future payment methods. Before the DCEP, according to the report of the Central Bank’s “Overall Payment System Operation in 2019”, we can see that China’s payment system is actually divided into two major blocks, the first is the central bank’s payment system, and the second is non-central bank payment system.

The two most important systems in the central bank system are:

One is called the large amount real-time payment system, referred to as the large-amount system. The large amount system processes a single credit business of more than 50,000 yuan, sends and clears it in real time, but only work between 8:30 and 17:00 on weekdays.

The other is called the small amount payment system, referred to as the small amount system. The single limit of the small amount system is 50,000 yuan, which is available every time. After a certain amount of time or accumulation, the payment bank and the collection bank calculate the net amount of the transaction between the two parties. The net amount will be submitted to the large amount system for settlement after the gap is exceeded.

Therefore, many banks’ online banking clients will remind users that if they want to transfer money during non-working hours, they must split the large amount of transfers into several 50,000 yuan or less to ensure fast arrival. The two most important systems in the non-central bank system are the bank card inter-bank payment system, referred to as the UnionPay system. The typical scenario is to use one bank ’s bank card to withdraw from another bank ’s ATM, or to pay through the bank ’s POS machine. At this time, it will be processed through the UnionPay system;

The other is that after the emergence of third-party payment technology, a new network-linked clearing platform, called the network-linked system, is now established. When we use third-party payment platforms like WeChat and Alipay to pay online, the third-party payment platform must be on the network-linked platform. A reserve account is opened inside. Large-amount system, small-amount system, UnionPay system, and network-linked system are currently the most important payment systems in China. According to the 2019 data, these four systems are calculated by the number of payments, accounting for 94%, and calculated by the amount of payment,occupying 78.8%. After the emergence of DCEP, it will bring a new pattern to China’s payment system. First of all, DCEP is a brand-new, completely independent system. Its core is called one currency, two banks and three centers.

One coin is the encrypted string representing the banknote issued by the central bank to ensure that the holder can use the central bank’s credit to redeem it at any time.

The two banks refer to the issuance treasury of the central bank and the bank treasury of commercial banks. Of course, if from the amount perspective, the above “two”means more than two banks, because there may be multiple commercial banks as second-tier institutions, DCEP is first issued by the central bank to commercial Banks, which are sent from commercial banks to the accounts of residents and users, do not do so for technical reasons, but to prevent commercial banks from being channelized and marginalized in the DCEP era.

The three centers include a registration center responsible for recording the entire process of DCEP issuance, transfer and withdrawal, an authentication center that centrally manages the identity of DCEP accounts, and a big data center that monitors the payment behavior of DCEP accounts and performs data analysis. So if you have DCEP in your hand, don’t use it to do illegal things, it is easy to be analyzed by the system.

Secondly, the payment method of DCEP is different from other traditional payment systems. There are several possible solutions for DCEP’s payment settlement. Among them, I think the most thorough one is the real-time full settlement mode, which is payment transfers will go to the issuance registration system of the central bank, that is, DCEP payment and settlement will be completely independent of the bank card system and third-party payment system.

For example, if you transfer 9 yuan to someone else’s WeChat account, you actually deducted 9 yuan from your WeChat payment account, and 9 yuan was added to someone else’s WeChat payment account. However, the payment with DCEP is different. It is also that you transfer 9 yuan DCEP to someone else. This process is like paying cash. You transfer to someone else a 10 yuan denomination of DCEP, and you receive a change of 1 yuan DCEP. In order to avoid revealing the user’s privacy through transaction records, there is another thing similar to the destruction and recasting of the privacy coin. DCEP’s issuance registration system invalidates the original 10 yuan of the payer and produces a new 9 yuan. The money is given to the payee, and the newly produced 1 yuan is given to the original payer for change.

DCEP itself supports smart contracts, and it has reserved a field for the script language of smart contracts, so it can achieve more functions than ordinary cash payments.

The Central Bank’s Digital Currency Research Institute described a very typical application scenario in the patent “201710496964.3 A digital currency-based investment financing transaction method, system and device”, replacing the current P2P center platform with digital currency based on smart contract script to transfer funds and handle payment and settlement of online lending activities of investors and fundraisers, to solve risks such as deposit of investor funds in traditional depository accounts, opaque capital flow, and trust in the platform itself.

Then we can imagine that since P2P network lending can be done with DCEP smart contracts, can all other complex, conditional, and time-sensitive transaction scenarios in the future be completed using DCEP smart contracts.

Judging from our current pilots in the four places, DCEP payments will first be applied in the scenario of small high-frequency payments. For example, we now see transportation subsidies and party fees in Suzhou, Starbucks and McDonald ’s in Xiong’an. Since China’s mobile payment penetration rate is already very high, the old people have already learned to use Alipay and WeChat to pay and collect money. In my opinion, the large-scale promotion of DCEP in our country should not take too long. In various industries, various application scenarios, and various large and small payment activities, DCEP will occupy an increasingly important position.

03 What does DCEP mean for blockchain practitioners?

After the release of DCEP, there will be a large-scale upgrade and transformation of three systems: The first is the central bank system. The central bank will completely build a new system for DCEP issuance, return, control and management, including systems that involve encoding and decryption, changes in ownership, etc. The current system is only used for internal testing, which is not enough from a complete, large-scale commercial-grade system, so this is the central bank ’s annual investment. Since this business involves the central bank’s core system, it is generally developed and maintained by the central bank’s self-built team, so no wasting for it. The second block is commercial banks and third-party payment companies that are second-tier institutions. They used to only have fiat currency account business. In the future, they must build a new DCEP management system. The original core system includes ATMs and POS. Such equipment also needs to be transformed, and is compatible with the legal currency account business and the DCEP business system. This business will have some traditional financial IT service companies to do unified system undertaking. Our private blockchain technology team may have the opportunity to get one of the module projects. The third block is the application chain and application-end systems of various industries, including B-side and C-side. We have talked about a lot of business on-chain and business contract in the past, and finally failed to solve the problem of trusted payment on the chain. As business on-chain and business contracting have not formed a closed loop, they have been developing slowly. But after the emergence of DCEP, the payment behavior itself can be controlled by smart contracts, then the closed-loop problem of the entire business can be solved well, so the development of various industrial chains and application chains will be greatly accelerated.

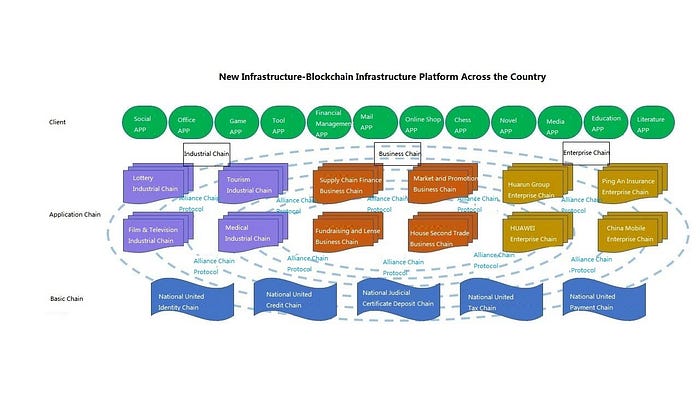

When the term “new infrastructure” came out last year, I drew a picture with the vision of the future blockchain basic platform I envisaged. At that time, the seven major directions of the new infrastructure were listed, and there was no clear statement about the inclusion of Blockchain, but when the National Development and Reform Commission introduced the new infrastructure on April 20 this year, it clearly stated that the blockchain infrastructure should be included in the new infrastructure planning. In this big idea, it is divided into three layers, namely the basic chain, the application chain, and the application side.

The basic chain is a public service chain that is promoted and led by the national level. DCEP can be regarded as a unified payment chain of the country. I think there will be a public identity chain, a public credit chain, and a public judicial deposit Chain, public tax chain.

The application chain can be divided into three categories, namely, the industry chain led by leading enterprises in various industries, the business chain jointly led by the core business constituent organizations, and the enterprises chain built independently by super large enterprises and large enterprises. Between each application chain and the basic chain, the chain link chain protocol, or what we call cross-chain protocol is used to achieve user access, data mutual trust, business interoperability, and smart contract interoperability.

In fact, the application side still maintains the user experience of our current mobile Internet APP. The APP interacts with the chain through the interface provided by the application chain, shields the user’s perception of the chain, and reduces the application threshold. The investment is at least 100 billion yuan for the complete establishment of this system. In terms of time, it will take at least 5–10 years. This is an opportunity for our domestic blockchain technology team, but everyone should also know that this is a hard work and technical work. The competition is the technical ability of each team, everyone’s understanding of the industry, applications, and business and the ability to deliver high-quality projects. I believe that in the next 3–5 years, there will be a group of domestic blockchain teams with deep technology that can stand out and become outstanding stars and outstanding representatives of domestic technology companies. Our brief introduction about DCEP today is basically over here, and finally we need to give a friendly reminder. Since DCEP is not officially released, today’s analysis of DCEP comes from our team’s research on the technical documents such as DCEP prototype reports and patents published online. If the research is different from the final DCEP system in some details, please refer to the official technical white paper. thank you all.

04 Q&A

Q: What kind of development will DC / EP usher in 2020? How does payment affect the currency?

A: From the trial of DCEP in four places to full-scale rollout, we do not expect this time to be too long. If it is slow, it will be 3–5 years, and if it is fast, 2–3 years. In the process of trial and promotion, the mandatory issuance of DCEP may be requested in some scenarios, such as subsidies, wages, medical insurance, etc.

At the same time, DCEP is also legally compensable. Merchants, businesses, and shopping malls must not refuse to accept DCEP. They must be able to have a DCEP collection device, which may be an APP wallet or a POS machine that supports DCEP. After the popularization of simple peer-to-peer payment functions, more complex applications that load different attributes and load smart contracts will soon appear. So it should be said that the next five years will be five years of DCEP application blowout.

Q: Is the central bank DCEP a blockchain application?

A: Many people have misunderstood DCEP. After reading several news reports, you may feel that DCEP is not a blockchain application, because DCEP ’s white paper and technical details have not been published. There are only some reports on prototype systems and nearly 100 copies of DCEP related technology patents, most people do not have the patience to do careful research.

If you study carefully, you can find that in fact, DCEP’s technical architecture in blockchain is more complicated than Libra, and at the same time it integrates many solutions to real-world currency and financial problems. If everyone thinks that libra is a blockchain application, then why can’t DCEP be regarded as a blockchain application. Bitcoin currently has a market value of more than 1 trillion yuan, and the M0 balance in 2019 is 7.7 trillion yuan. If DCEP can account for 15–20% of M0 in the future, it will have surpassed Bitcoin as the largest application of the blockchain.